Unit-Linked Investment in Portugal

A Unit-Linked product is a life insurance contract connected to investment funds. Instead of placing your long-term capital into a generic savings account, your premium is converted into investment units linked to professionally managed funds, with the allocation selected according to your objectives, time horizon and tolerance for market volatility.

Unit-Linked Products - Portugal

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationWhy Choose a Unit-Linked Investment Plan?

Because long-term capital should be structured, diversified and actively positioned, not left idle.

Leaving capital in a low-yield current account may feel comfortable, but over time it can lose purchasing power when inflation is higher than the interest received. A Unit-Linked investment plan offers a more strategic alternative: your money is placed inside an insurance-based investment structure and allocated to professionally managed funds selected according to your objectives, time horizon and risk profile.

With a Unit-Linked plan, the goal is not to promise a fixed return. The goal is to give your savings access to diversified investment strategies, including bond, multi-asset and equity funds, while keeping the investment wrapped inside a life insurance contract. This allows the client to combine market participation, beneficiary planning and long-term tax positioning in one structure.

For clients who want to move beyond passive cash savings, Unit-Linked products can be especially relevant because they offer:

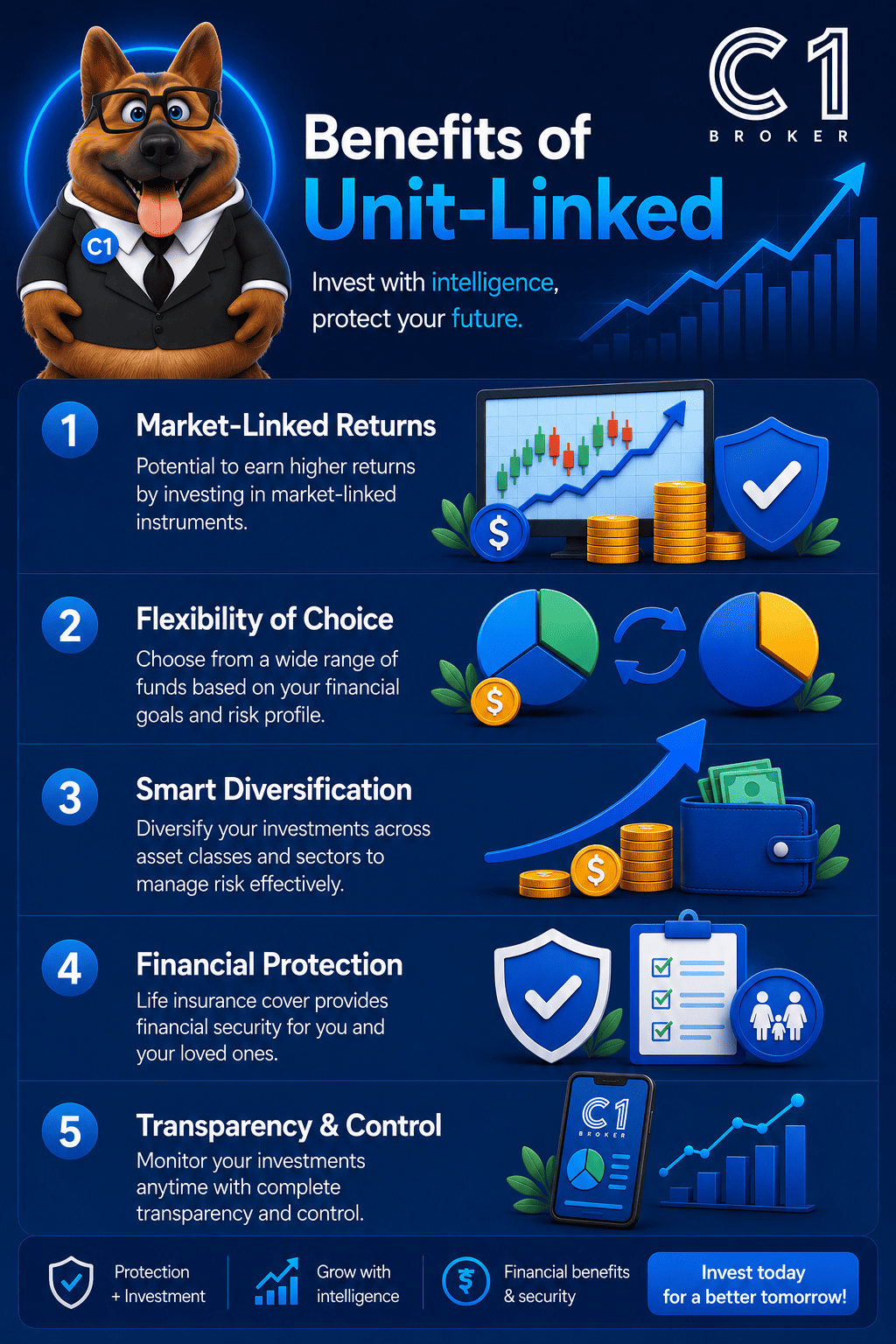

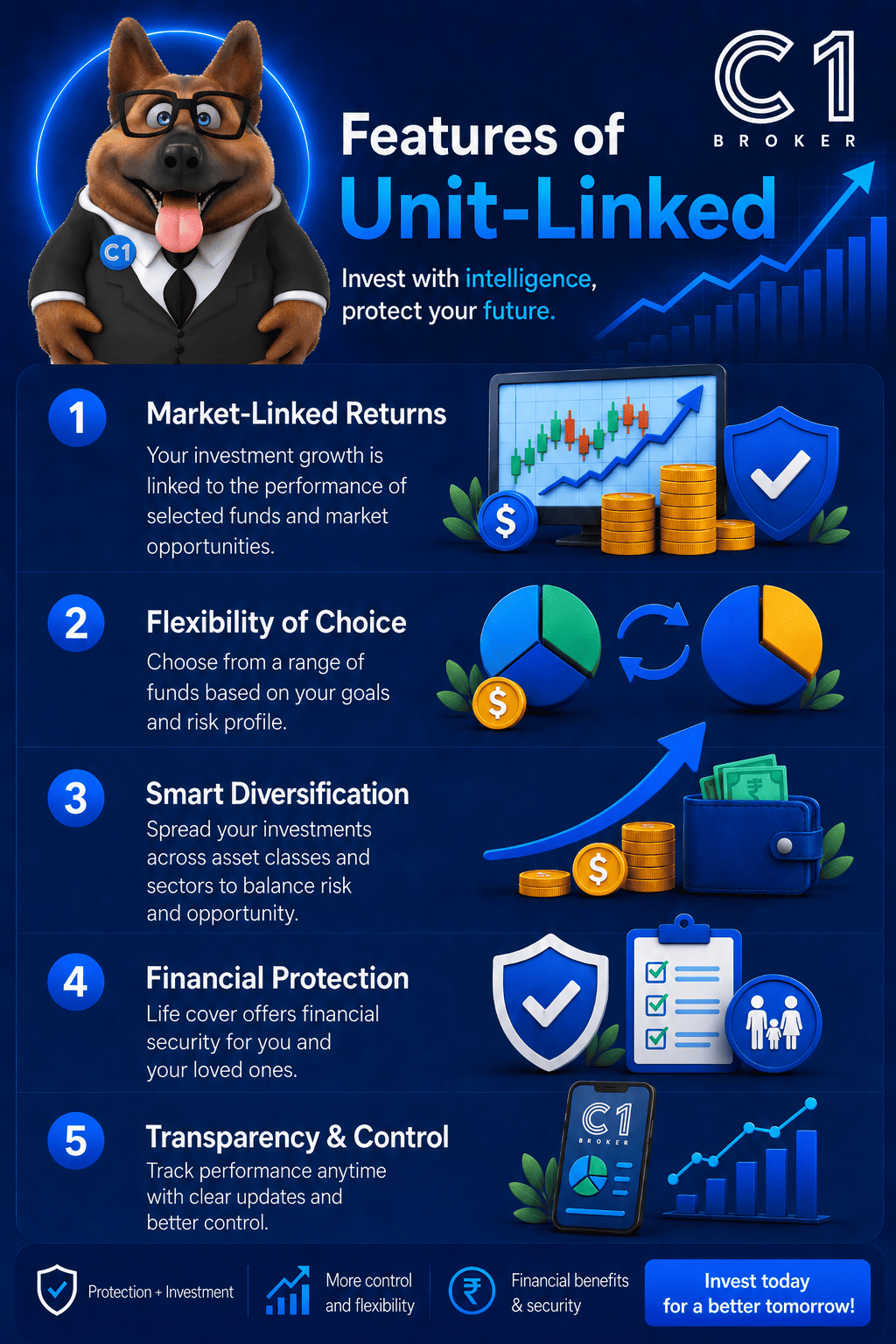

- Market-linked growth potential — your investment is connected to fund performance, rather than limited to traditional bank deposit interest.

- Professional fund management — Allianz Investimento gives access to strategies managed by recognised asset managers such as Allianz Global Investors, PIMCO and JP Morgan.

- Flexible investment formats — clients may choose between a single premium investment or regular contributions, depending on their planning needs.

- Long-term tax efficiency — under the Portuguese decreasing tax scale for Unit-Linked and capitalization insurance contracts, gains may be taxed at 28%, 22.4% or 11.2%, depending on the holding period and legal contribution conditions.

- Beneficiary protection — in the event of the insured person’s death, Allianz Investimento may pay the designated beneficiaries the market value of the fund units plus an additional amount equal to any depreciation, according to the contractual rules.

- Strategic fund switching — transferring capital between open-ended funds inside a Unit-Linked contract can be done without triggering an immediate taxable capital gains event inside the policy structure.

At C1 Broker, we do not treat Unit-Linked products as a generic investment. We assess whether the structure is appropriate for the client first, then analyse the suitable investment profile and fund options. The right question is not only “which fund should I choose?” The first question is: does this market-linked insurance structure fit my objectives, risk tolerance and investment horizon?

Choose Your Unit-Linked Profile: Conservative, Balanced or Aggressive

One insurance structure. Three investor profiles. Eight fund options.

A Unit-Linked investment plan gives you access to market-linked funds through an insurance-based structure. The key decision is not simply which fund looks attractive. The first decision is which investor profile matches your financial behaviour.

With Allianz Investimento, the available fund range is divided into three clear profile categories:

- Conservative Profile — for investors who prioritise lower volatility and want to avoid high fluctuations.

- Balanced / Moderate Profile — for investors who accept some market movement in exchange for stronger medium-term growth potential.

- Aggressive Profile — for long-term investors who prioritise capital growth and can tolerate significant market fluctuations.

The Allianz Unit-Linked fund universe currently includes 8 open-ended fund options: 2 Conservative funds, 2 Balanced / Moderate funds, and 4 Aggressive funds. These range from bond-focused and multi-asset strategies with 0% to 15% equity exposure, to growth-oriented equity strategies with 75% to 100% equity exposure.

.

.

Read More About The Investments Profiles in Our Post.

3 Unit-Linked Profile / Plans Options

Start with your risk level before selecting the funds.

Allianz Investimento offers three Unit-Linked investment profiles, each designed for a different level of market exposure, volatility tolerance and long-term return objective.

Conservative

Lower volatility. Controlled market exposure.

For clients who want market participation but prefer to reduce large fluctuations. This profile uses bond and low-equity multi-asset strategies.

- 2 fund options Equity exposure: 0% to 15%

Moderate

Diversified growth with moderate risk.

For investors who accept some market movement in exchange for stronger medium-term growth potential through diversified multi-asset funds.

- 2 fund options Equity exposure: 30% to 50%

Agressive

Higher equity exposure for long-term growth.

For long-term investors focused on capital growth and comfortable with stronger market fluctuations during the investment period.

- 4 fund options Equity exposure: 75% to 100%

* Unit-Linked products are market-linked: capital is not guaranteed, values may rise or fall, and each profile reflects a different level of risk, volatility and growth potential.

Conservative Unit-Linked Profile

For investors who prioritise stability, lower volatility and controlled exposure to financial markets.

The Conservative Profile is designed for clients who want their capital to participate in professionally managed investment funds, but who do not want high exposure to equity-market fluctuations. This profile may be suitable for investors who value security, prefer a smoother investment journey and want to avoid large negative movements whenever possible.

This does not mean the investment is risk-free. Conservative Unit-Linked funds are still exposed to financial markets, especially bond-market risk, interest-rate movements and credit conditions. However, compared with the Balanced and Aggressive profiles, the Conservative Profile uses lower equity exposure and more defensive fund structures.

Conservative Profile Fund Options

| Fund | ISIN | Type | Category | Equity Exposure |

|---|---|---|---|---|

| PIMCO EURO INCOME BOND “E” | IE00B3QDMK77 | Open-ended | Global Bond Fund | 0% |

| ALLIANZ DYNAMIC MULTI SRI 15 “CT2” EUR | LU1462192250 | Open-ended | Global Multi-Asset Fund | 15% |

How the Conservative Funds Work

PIMCO EURO INCOME BOND “E”

This fund is the most defensive option in the Allianz Investimento range because it has 0% equity exposure. Its role is to give the client access to a professional bond strategy rather than direct exposure to the stock market. For investors who want a lower-volatility Unit-Linked allocation, this type of fund can help reduce the impact of equity-market declines.

However, bond funds are not the same as guaranteed deposits. They can still fluctuate due to interest-rate changes, bond prices, credit spreads and market liquidity. The advantage is not a capital guarantee; the advantage is a more defensive investment structure compared with equity-heavy strategies.

ALLIANZ DYNAMIC MULTI SRI 15 “CT2” EUR

This fund introduces a small equity component, with 15% equity exposure, while remaining primarily defensive. It is a global multi-asset strategy, meaning it can combine different types of assets rather than relying only on one market segment.

This fund may be appropriate for clients who want slightly more growth potential than a pure bond allocation, but who still want to remain within a conservative framework. The equity exposure is limited, which helps control volatility, while the multi-asset structure gives the portfolio broader diversification.

Conservative Profile — Best Fit

This profile may be suitable for clients who:

- Want a Unit-Linked investment structure but prefer lower market fluctuation.

- Have a cautious approach to risk.

- Prefer bond or low-equity multi-asset exposure.

- Want to begin investing without moving directly into high-equity funds.

- Accept that returns may be more moderate than in higher-risk profiles.

.

.

Read More in Our Conservative Profile Post.

Moderate Unit-Linked Profile

For investors seeking diversified growth with a controlled level of risk.

The Balanced Profile, which may also be presented on the website as the Moderate Profile, is designed for investors who want stronger growth potential than a conservative allocation, but who still want diversification and risk control. It may suit clients who understand that markets fluctuate and who can accept occasional losses in exchange for higher medium-term investment growth potential.

This profile is built around global multi-asset funds. That means the investment is not concentrated only in shares or only in bonds. Instead, the portfolio combines asset classes, allowing the client to participate in market growth while still keeping part of the allocation outside full equity exposure.

Balanced / Moderate Profile Fund Options

| Fund | ISIN | Type | Category | Equity Exposure |

|---|---|---|---|---|

| ALLIANZ DYNAMIC MULTI SRI 30 “CT2” EUR | LU2829845630 | Open-ended | Global Multi-Asset Fund | 30% |

| ALLIANZ DYNAMIC MULTI SRI 50 “CT2” EUR | LU1462192417 | Open-ended | Global Multi-Asset Fund | 50% |

How the Moderate Funds Work

ALLIANZ DYNAMIC MULTI SRI 30 “CT2” EUR

This fund sits at the lower end of the Balanced / Moderate range, with 30% equity exposure. It may be appropriate for clients who want more return potential than a conservative strategy but are not yet comfortable with a portfolio where half or more of the investment is exposed to equities.

The 30% equity allocation gives the fund access to market growth, while the remaining non-equity allocation helps reduce full stock-market dependency. This makes it a useful middle-ground option for investors moving from a cautious position into a more growth-oriented structure.

ALLIANZ DYNAMIC MULTI SRI 50 “CT2” EUR

This fund has 50% equity exposure, making it the more growth-oriented option within the Balanced / Moderate profile. It is still a global multi-asset fund, but the higher equity allocation means the investor should expect more fluctuation than with the 30% version.

This option may be suitable for clients with a medium- to long-term investment horizon who are willing to accept more volatility in exchange for stronger capital growth potential. It can work well for investors who do not want a fully aggressive equity strategy, but who also do not want their capital positioned too defensively.

Balanced / Moderate Profile — Best Fit

This profile may be suitable for clients who:

- Want a balance between risk control and growth potential.

- Accept moderate market fluctuations.

- Prefer diversified multi-asset funds.

- Have a medium- to long-term investment horizon.

- Want higher growth potential than the Conservative Profile without moving fully into equity-heavy funds.

.

.

Read More in Our Moderate Profile Post.

Aggressive Unit-Linked Profile

For long-term investors focused on capital growth and comfortable with higher volatility.

The Aggressive Profile is designed for investors whose main priority is long-term capital growth. This profile accepts stronger market fluctuations during the investment period because it uses higher equity exposure. It may be suitable for clients with a longer investment horizon, higher risk tolerance and the emotional capacity to remain invested during market downturns.

This is the profile with the widest fund selection in the Allianz Investimento range. It includes one high-equity multi-asset fund and three full-equity strategies, giving investors access to global, North American and European equity markets.

Aggressive Profile Fund Options

| Fund | ISIN | Type | Category | Equity Exposure |

|---|---|---|---|---|

| ALLIANZ DYNAMIC MULTI SRI 75 “CT2” EUR | LU1462192680 | Open-ended | Global Multi-Asset Fund | 75% |

| ALLIANZ BEST STYLES GLOBAL EQUITY SRI CT EUR | LU3049577607 | Open-ended | Global Equity Fund | 100% |

| JPM US SELECT EQUITY PLUS A | LU0281483569 | Open-ended | North American Equity Fund | 100% |

| JPM EUROPE EQUITY PLUS | LU0289089384 | Open-ended | European Equity Fund | 100% |

How the Aggressive Funds Work

ALLIANZ DYNAMIC MULTI SRI 75 “CT2” EUR

This fund is the bridge between a diversified multi-asset strategy and a high-growth equity allocation. With 75% equity exposure, it is clearly growth-focused, but it is not a pure equity fund. The remaining allocation gives it a degree of diversification outside equities.

This may be suitable for investors who want aggressive growth potential but still prefer a multi-asset structure rather than a 100% equity fund. It can be seen as the first step inside the Aggressive Profile before moving into fully equity-based strategies.

ALLIANZ BEST STYLES GLOBAL EQUITY SRI CT EUR

This is a 100% global equity fund, meaning the investment is fully exposed to stock markets. Its global structure allows the investor to access companies across different regions and sectors, rather than focusing only on one geographic market.

Because it is fully equity-based, this fund can fluctuate significantly. It may be suitable for long-term investors who want broad global equity exposure and who understand that short-term market declines are part of the investment journey.

JPM US SELECT EQUITY PLUS A

This fund provides 100% equity exposure to the North American market. It is suitable for investors who want specific access to US and North American companies, which can be attractive for clients who believe in the long-term strength of that region’s corporate market.

However, because this fund is regionally focused, it carries concentration risk. If the North American equity market underperforms, the fund may be more affected than a globally diversified equity fund. It should therefore be selected only when the client understands the risks of regional equity exposure.

JPM EUROPE EQUITY PLUS

This fund provides 100% equity exposure to European markets. It may be used by investors who want direct participation in European companies and who want to diversify away from a purely US-focused equity allocation.

As with any full-equity strategy, the fund can experience strong upward and downward movements. It may be suitable for long-term investors who want exposure to European market opportunities and who are comfortable with regional equity volatility.

Aggressive Profile — Best Fit

This profile may be suitable for clients who:

- Have a long-term investment horizon.

- Prioritise capital growth over short-term stability.

- Accept strong market fluctuations.

- Understand that equity funds can fall significantly during market corrections.

- Want access to global, North American and European equity strategies.

- Are comfortable investing through funds with 75% to 100% equity exposure.

.

.

Read More in Our Agressive Profile Post.

“With a Unit-Linked investment plan, your capital is not left idle, it is allocated to professionally managed funds according to your risk profile, investment horizon and long-term objectives. To understand which profile may suit you best, contact our team at C1 Broker.”

Allianz + C1 Broker: Confidence You Can Feel

Unit-Linked investments require more than simply choosing a fund. Because the investment value depends on financial markets, the quality of the structure, the fund selection process and the client’s risk assessment all matter.

With Allianz Investimento, clients can access a medium- to long-term Unit-Linked solution connected to recognised asset managers such as Allianz Global Investors, PIMCO and JP Morgan. The product is designed for individuals and companies who want an investment structure that can adapt to their risk profile, contribution format and long-term planning objectives.

At C1 Broker Portugal, our role is to help you understand the structure before you invest: how the product works, which profile may be suitable, what risks are involved, how liquidity works, and how each fund option fits into your overall strategy.

.

The Strength of Allianz Investimento

Allianz Investimento combines the legal structure of life insurance with access to investment funds. The premium is converted into investment units, and the value of the policy follows the performance of the selected funds.

This structure allows clients to choose between single premium investment and regular contributions, while building a portfolio according to their Conservative, Balanced or Aggressive profile.

The product also includes an important protection mechanism in the event of death: beneficiaries may receive the market value of the fund units plus an additional amount equal to any depreciation, subject to the contractual rules defined by Allianz.

.

The Role of C1 Broker

C1 Broker does not position Unit-Linked products as a generic savings account or a guaranteed-return solution. Our role is to guide the client through a technical decision-making process.

We help clarify:

- which investment profile is appropriate;

- whether a single premium or regular contribution plan makes more sense;

- how much volatility the client can realistically tolerate;

- how each fund category fits the client’s time horizon;

- when a Unit-Linked structure may be preferable to direct fund ownership or traditional bank savings.

This is especially important because Unit-Linked products involve financial market risk. The policyholder bears the investment risk, including volatility, credit risk and liquidity risk.

.

Independent Advice Before Fund Selection

The fund should never be the first decision. The first decision is whether the Unit-Linked structure itself is appropriate for your objectives.

Only after that should the client move into profile selection: Conservative, Balanced or Aggressive. Allianz Investimento currently offers 8 open-ended fund options, ranging from a 0% equity bond fund to 100% equity strategies across global, North American and European markets.

At C1 Broker, we make this process clear, structured and transparent, so the client understands not only the potential upside, but also the risks, limitations and long-term responsibilities of investing through a Unit-Linked product.

Yes, I Want to Structure My Unit-Linked Investment Plan

Your long-term capital deserves a clear strategy, not guesswork.

With a Unit-Linked investment plan, your money can be allocated to professionally managed funds according to your risk profile, time horizon and growth objectives.

FAQs

Frequently Asked Questions about the Allianz Active PPR

A Unit-Linked product is a life insurance contract connected to investment funds. The premium is converted into investment units, and the value of the contract changes according to the performance of the selected funds. It is not a bank deposit or a fixed-interest savings account.

To understand whether a Unit-Linked structure fits your objectives, contact C1 Broker’s investment team here.

No. Unit-Linked products are market-linked, which means the value may rise or fall. The financial market risk, including volatility, credit risk and liquidity risk, is borne by the policyholder.

To review whether this level of risk is appropriate for your situation, contact C1 Broker’s investment team here.

They may be suitable for clients looking for a medium- to long-term investment structure, with access to professionally managed funds and a risk profile adapted to their objectives. They are not suitable for clients who require guaranteed capital or short-term certainty.

To better understand which investor profile may fit your situation, complete C1 Broker’s Investor Profile Test.

Investment options are generally structured around three primary risk profiles—Conservative, Balanced, and Aggressive—to match different financial goals and risk tolerances. The Conservative profile focuses on capital preservation by minimizing large market fluctuations, the Balanced profile accepts moderate volatility in exchange for steady growth potential, and the Aggressive profile prioritizes high long-term returns by accepting significant market variations along the way.

.

To understand your own risk tolerance before selecting a Unit-Linked fund, complete C1 Broker’s Investor Profile Test.

The Allianz Investimento range includes 8 open-ended fund options: 2 Conservative funds, 2 Balanced funds and 4 Aggressive funds. These range from a 0% equity bond fund to 100% equity funds focused on global, North American and European markets.

To better understand how risk profiles should guide fund selection, read C1 Broker’s guide on investor risk profiles before investing in Portugal here.

Possibly, but only if it matches your risk tolerance, investment horizon and ability to accept market losses. The Aggressive profile may offer higher long-term growth potential, but it also involves higher volatility and a greater risk of temporary or permanent loss.

To understand whether this profile fits your investment behaviour, read C1 Broker’s guide to the Aggressive Investor Profile in Portugal here.

Before subscribing, clients should review the official Allianz documentation, including the Pre-Contractual Information, Key Information Document, General Conditions, risk information, fees, sustainability disclosures and fund documentation. This helps ensure the decision is made with full transparency.

To understand how Unit-Linked products fit within the wider savings and investment options available in Portugal, visit C1 Broker’s Savings & Investments page.

They can be tax-efficient when held over the medium to long term. Under the Portuguese decreasing tax scale for Unit-Linked and capitalization insurance contracts, capital gains may be taxed at 28%, 22.4% after 5 to 8 years, or 11.2% after more than 8 years, provided the legal contribution timing conditions are met.

To compare Unit-Linked tax treatment with other savings and investment structures in Portugal, visit C1 Broker’s Savings & Investments page.

In the event of death, the designated beneficiaries may receive the market value of the fund units plus an additional amount equal to any depreciation, if depreciation exists and according to the contractual rules defined by Allianz.

To better understand how Unit-Linked products can support beneficiary planning, speak with C1 Broker’s investment team here.

C1 Broker helps clients understand the product structure, compare the available profiles, assess the risks, review the documentation and select a strategy aligned with their objectives. The goal is not to push one profile, but to guide the client toward a suitable Unit-Linked structure based on risk tolerance, time horizon and financial goals.

To begin with a broader view of savings and investment options in Portugal, visit C1 Broker’s Savings & Investments page.

Allianz Unit-Linked Documents

At C1 Broker, we believe every investment decision should be made with full clarity. Below you can access the essential Allianz documentation for the Unit-Linked product, including general conditions, product information, investment features, risk details and applicable costs.

.

Please review these documents carefully before subscribing. Unit-Linked products are linked to financial markets, may fluctuate in value and should be assessed according to your risk profile, investment horizon and financial objectives.

Allianz Unit-Linked Documents

- Pre-Contractual Information (Informação Prévia à Contratação)

- Key Information Document (Documento de Informação Fundamental)

- Allianz Investimento Glossary (Glossário Allianz Investimento)

- Transparency in the Integration of Sustainability Risks (Transparência na Integração dos Riscos de Sustentabilidade)

Start Investing Today!

The information provided on this page is for general informational, educational and commercial purposes only and is intended to present, in broad terms, insurance-based savings and investment solutions, including Retirement Savings Plans (PPRs), Unit Linked life insurance products, capitalisation contracts and other medium- or long-term savings structures distributed through insurance channels. This information does not constitute financial, investment, tax or legal advice, nor does it constitute a personalised recommendation to subscribe, maintain, modify, transfer, switch, redeem or surrender any product.

PPRs and Unit Linked products may involve risks, including market risk, liquidity risk, credit risk, currency risk, interest rate risk, inflation risk, counterparty risk, operational risk, regulatory risk and the risk of partial or total loss of the capital invested. Unless an express guarantee is provided in the contractual terms and conditions of the product, neither the invested capital nor the return is guaranteed. The value of the investment may rise or fall, and past performance is not a reliable indicator of future results.

Insurance-based savings and investment products are not equivalent to bank deposits and should not be understood as risk-free savings accounts. Depending on the product structure, the value payable to the policyholder, insured person or beneficiary may depend, directly or indirectly, on the performance of underlying funds, financial markets, reference assets, units of participation or the investment policy defined by the insurance undertaking or product manufacturer. Any capital protection, death benefit, beneficiary clause, guaranteed rate, minimum return, depreciation compensation or other protection mechanism applies only where expressly provided in the official contractual documentation and subject to the limits, exclusions, valuation rules and conditions stated therein.

Where the product is linked to investment funds or other market-exposed assets, the financial risk is generally borne, in whole or in part, by the policyholder or investor. Redemptions, partial withdrawals, transfers, switches, cancellations or early surrenders may be subject to contractual restrictions, valuation dates, settlement periods, minimum holding periods, commissions, penalties, market value adjustments, minimum remaining balances or temporary liquidity limitations. In periods of market stress, exceptional volatility, suspension of underlying funds or operational disruption, redemption or switching may be delayed, restricted or processed at a value different from that expected by the client.

Any reference to tax benefits, reduced taxation, PPR deductions, favourable redemption regimes or long-term fiscal advantages is provided only as general information based on the legislation understood to be applicable at the date of publication. Tax treatment may depend on the client’s tax residence, age, personal circumstances, annual IRS position, product type, contribution history, holding period, redemption reason and compliance with the legal conditions in force. Tax law, administrative interpretation and reporting obligations may change over time, and any tax advantage may be reduced, suspended, withdrawn or lost where the applicable legal or contractual conditions are not met.

Before subscribing to any product, the client must carefully read all applicable pre-contractual and contractual documentation, including, where applicable, the Key Information Document (KID/DIF), the Information Note, the General, Special and/or Particular Conditions, information on risks, costs and charges, the investment policy, recommended holding period, surrender/redemption conditions and applicable tax regime. Any subscription decision must be made consciously and on an informed basis, taking into account the client’s investment objectives, knowledge and experience, financial situation, ability to bear losses, investment horizon and risk tolerance.

The subscription of insurance-based investment products is subject to the legally required suitability or appropriateness assessment, acceptance by the insurance undertaking and the specific terms and conditions of each product. The tax treatment of PPRs and other savings or investment products depends on the personal circumstances of the client and on the tax legislation in force, which may change over time. Early redemptions, transfers or contractual changes may result in penalties, charges, loss of tax benefits or other tax consequences.

C1 Broker® is a commercial brand of Wiseg Mediación de Seguros, S.L., an insurance brokerage authorised to distribute Life and Non-Life insurance, DGSFP Code J-3790, authorised to operate in Portugal through branch registration no. ASFFP 923047667. C1 Broker may receive remuneration from insurance undertakings for the distribution of insurance products, namely through commission included in the premium or product value, without prejudice to its duty to act honestly, fairly, professionally and in the best interests of the client. The client may request additional information on the nature and amount of the applicable remuneration.

For further information, personalised clarification or access to the legal documentation of any product, please contact C1 Broker before making any subscription decision.